Market Outlook: AI Rally to Return in the Second Half of 2026

3 Minute read

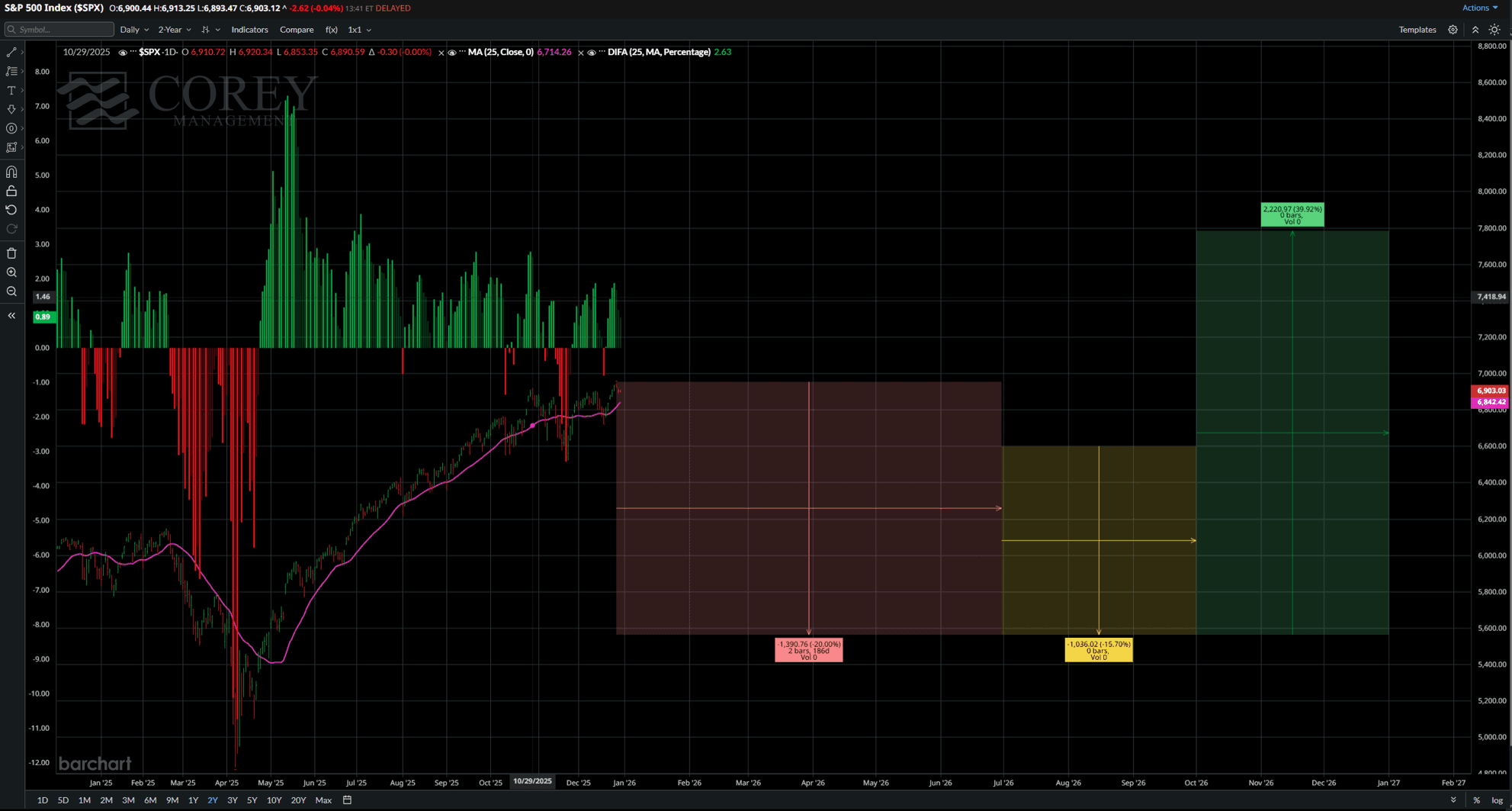

Our 2026 market outlook, forecasting heightened volatility and a potential 15-20 % pullback in the S&P 500 in the first half of the year.

Market Outlook: Waiting for the AI Rally to Return in the Second Half of 2026

Following a strong equity market in 2025, we expect increased volatility at the start of 2026 and foresee a substantial correction. Our base case anticipates a 15-20 % decline in the S&P 500 by the second quarter (approximately 5,500-5,200). We view this as a valuation-driven reset after significant multiple expansion, rather than a signal of collapse.

Key Drivers of Volatility

We see several macro catalysts that could contribute to turbulence in early 2026:

Supreme Court Tariff Decision (January–February): Markets will need to adjust to the ruling on tariffs linked to the Trump administration.

Labor Market Data (Spring): Labor reports may rekindle recession fears.

Federal Reserve Leadership Test (May): It will be the first significant test of the new Fed leadership.

U.S. Midterm Elections (November): We anticipate political uncertainty persisting until election results clarify fiscal and monetary policy direction.

Structural Volatility and AI Sentiment

Volatility Trend: Since August 2024, volatility has been trending upward. We expect Q1-Q3 2026 to show higher volatility alongside declining markets.

AI Stocks Sentiment: Although AI drove the 2025 rally, sentiment remains negative. We view this as a valuation or sentiment issue, not a fundamental one; order backlogs remain large, margins strong, and AI industrialization continues.

Valuation Dislocation: The market is grappling with pricing AI leaders after the initial enthusiasm. Investors are searching for a new consensus, which is taking time to form.

Outlook for Stability

Timing: We believe stability will not return before Q4 2026, when political uncertainty diminishes and fiscal and monetary policies align.

Valuation Concerns: With forward P/E ratios near record highs, we see limited upside from further multiple expansion.

Sector Rotation: Gains in late 2025 were driven by rotations into healthcare and banking, with a strong May-October stretch. We deem a repeat of this pattern unlikely in 2026.

Investment Strategy

Opportunity in Weakness: We encourage viewing the first half of 2026 as a chance to accumulate high-quality stocks at discounted prices, anticipating improving AI sentiment.

Focus Areas:

AI Infrastructure (chips, networking, hybrid hardware/software solutions)

High-Margin AI Components

Edge AI (inference directly on end devices)

High-Speed Connection Technology (No current recommendations due to over-saturation on amere of companies and price sensitivity of products).

Edge Devices: We see growing importance in inference on devices and automotive platforms.

Stocks to Watch

Broadcom Inc. (AVGO): Infrastructure Giant

Revenue Visibility: AI revenue increased 74 %, now nearly 60 % of semiconductor revenue.

Order Backlog: With a $73 billion backlog, we see strong long-term revenue visibility.

Market Leadership: Broadcom dominates networking and custom silicon for hyperscalers; another $1 billion order in 2026 further supports its lead.

Advanced Micro Devices (AMD): Strategic Challenger

Perception vs. Reality: We see AMD penalized by doubts over AI spending sustainability, yet its fundamentals remain solid.

OpenAI Partnership: A 6 GW commitment underscores AMD’s credibility within the AI ecosystem.

Focus on Bottlenecks: Management is addressing power and packaging constraints rather than focusing solely on compute demand.

Financial Discipline: With gross margins around 55-58 % and a 20 % pullback from highs, we expect AMD to recover by late 2026.

Qualcomm Inc. (QCOM): Underrated Edge AI Winner

Edge AI Expertise: Qualcomm excels in low-power inference on devices and in vehicles.

Automotive Growth: Automotive revenue grew 36 % to a $4 billion annual run rate, showing diversification beyond smartphones.

Valuation Support: Trading around 15× expected earnings, Qualcomm is supported by $3.4 billion in quarterly buybacks and dividends, offering growth at an attractive price.

Conclusion

In our view, the AI boom is far from over; it simply needs time for expectations to reset. Early 2026 volatility should be seen as the necessary “price of admission” for the next leg of the AI-driven cycle, which we anticipate will gain momentum in the second half of the year. We recommend using the first half of 2026 to build positions in high-quality AI-focused companies poised to lead the next wave of innovation.

Disclaimer

The opinions and analysis presented in this outlook are provided solely for informational purposes and reflect our collective views at the time of writing. They do not constitute personalized investment advice or recommendations. Markets and economic conditions can change rapidly, and past performance does not guarantee future results. We encourage you to conduct your own research and consult a qualified financial advisor before making any investment decisions.

Advisory-led.

Investment-ready within one week.

Strategies

Legal

Investors

KYC - Process

Mandate

Partnership

Equity Participation / Shareholding

Confidential Disclosure Agreement

Contact Us

© 2025 COREY Management | All rights reserved