U.S. Bonds in Focus: A Possible Trigger for Equity Market Weakness.

5 Minute read

Why the U.S. Bond Market could be „THE TRIGGER“ for the next equity market decline.

Market Structure and Repricing Dynamics

In our most recent market outlook dated December 31, 2025, we analyzed rising volatility within the prevailing market structure and identified the emergence of a new repricing cycle among technology equity investors, particularly in AI and software companies. This assessment remains unchanged and is currently being further reinforced by ongoing market developments.

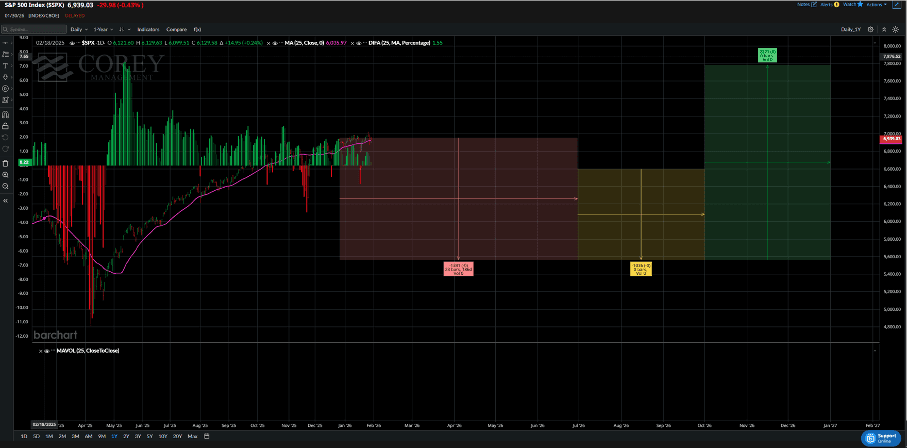

Equity Market Consolidation at Elevated Levels

Despite new technical all-time highs in the S&P 500 and NASDAQ, equity markets are currently consolidating at elevated levels. The largest-capitalization companies are trading sideways to lower, while the broader market continues to show sideways to moderately rising price action. Against this backdrop, we remain confident in our outlook for a 15-20 percent decline in the S&P 500, corresponding to levels of approximately 5,500 to 5,200.

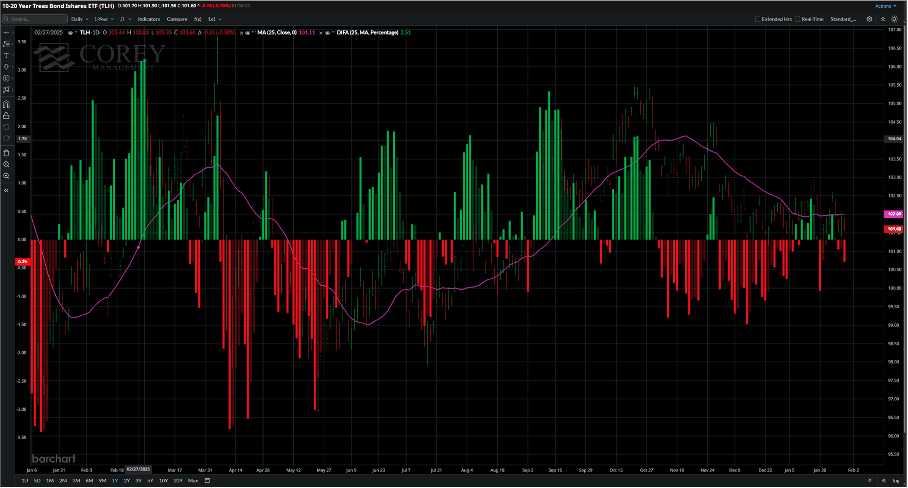

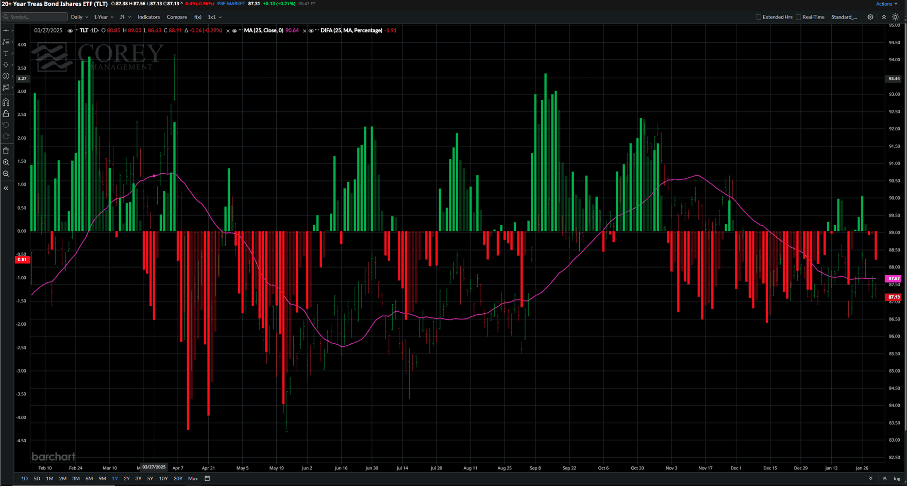

Liquidity Signals from Precious Metals and Bond Markets

Following the recent price declines in precious metals markets, earlier increases in margin requirements, widening precious metals spreads across trading venues, and a broad consolidation across bond markets, we see a realistic scenario of a liquidity-driven price decline in U.S. bond markets over the next four to twelve weeks. Bond markets are currently awaiting further guidance from the Federal Reserve and are showing subdued price action with a clear sideways bias. Investors who accumulated bonds in the fourth quarter of 2025 in anticipation of further declines in interest rates have, for now, seen little reward and may begin to display weakening conviction.

U.S. Bonds as a Potential Catalyst for Equity Market Weakness

Declining bond prices would place broad-based pressure on equity markets and could act as the trigger for a downward trend extending into the second quarter of 2026. Companies with elevated debt levels and upcoming material refinancing needs would likely be among the primary losers. This would also include AI-related companies that rely on long-term infrastructure financing. At the same time, neither record-breaking market-wide earnings growth nor growth in line with current estimates appears likely to provide a sufficient counterbalance to stabilize equity markets.

Macroeconomic and Geopolitical Headwinds

From a geopolitical perspective, recent progress in peace negotiations between Ukraine and Russia does not constitute a meaningful stabilizing catalyst, particularly in light of the newly reignited negotiations surrounding Greenland. As a result, a broadly stable situation in Europe does not appear to be within reach in the near term.

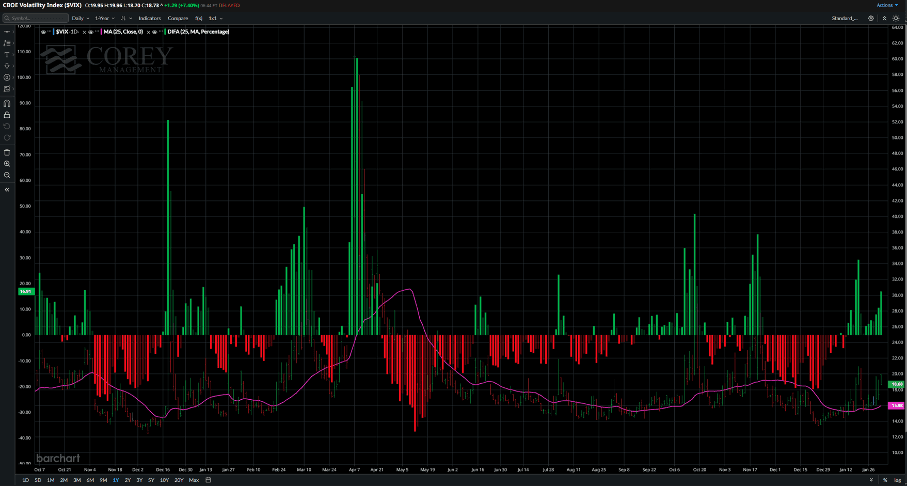

Rising Volatility as a Structural Feature

Against this backdrop, it is unsurprising that the trend of rising volatility, as reflected by the VIX, is expected to persist.

Policy Response and Medium-Term Market Implications

A declining bond market would, however, represent a constructive medium-term catalyst for equity markets. It would create an attractive entry opportunity in long-dated U.S. Treasuries and simultaneously increase pressure on the Trump administration and the Federal Reserve to act in closer coordination. Such a scenario would likely result in renewed monetary expansion, interest rate cuts of up to 100 basis points, and a further de-escalation or halt of tariff-related threats by the U.S. administration.

Conclusion: Positioning for Volatility and Opportunity

In summary, we maintain our existing forecasts and extend them to include the risk of declining bond prices. In our view, falling bond prices would likely prompt swift intervention by the U.S. government and the Federal Reserve, laying the foundation for a more stable environment for equity markets from the third quarter of this year onward. Under such conditions, AI-related equities would offer particularly attractive valuations, while investment strategies that benefit from elevated volatility are expected to remain structurally advantaged.

Disclaimer

The opinions and analysis presented in this outlook are provided solely for informational purposes and reflect our collective views at the time of writing. They do not constitute personalized investment advice or recommendations. Markets and economic conditions can change rapidly, and past performance does not guarantee future results. We encourage you to conduct your own research and consult a qualified financial advisor before making any investment decisions.

Advisory-led.

Investment-ready within one week.

Strategies

Legal

Investors

KYC - Process

Mandate

Partnership

Equity Participation / Shareholding

Confidential Disclosure Agreement

Contact Us

© 2025 COREY Management | All rights reserved